What is the best way to pay yourself this year? In this post, we break down the most tax efficient directors salary for 2024/25. If you’d like individualised help with this, get in touch with us today.

The basics

In last year’s Tax Efficient Directors Salary 2023/24 post, we explained that the most tax efficient salary UK directors could pay themselves when using a strategic mix of salary and dividend payments. This remains true for 2024/25. For this year’s mix, we recommend including the basic salary component because this:

- Will incur little to no National Insurance contributions.

- Will leverage your annual Personal Tax-Free Allowance.

- Is an allowable business expense for your company, which may well lower your corporation tax.

The remainder of your income can be earned through dividend payments because these are subject to the lower dividend tax rates. We will focus on the salary component in this article, but you can learn more about dividends here.

What this article assumes

So, what is the most tax efficient salary? When discussing this, we have to create a baseline. To that end, this article assumes that you have no other income from any other sources (e.g., other employment, property, or investment). The reason for this is that if you do have other income then that may already be using your tax-free allowances, which may change the most tax efficient salary and dividend mix. This will be more clear when you understand the allowances and thresholds which apply to your OVERALL income this year.

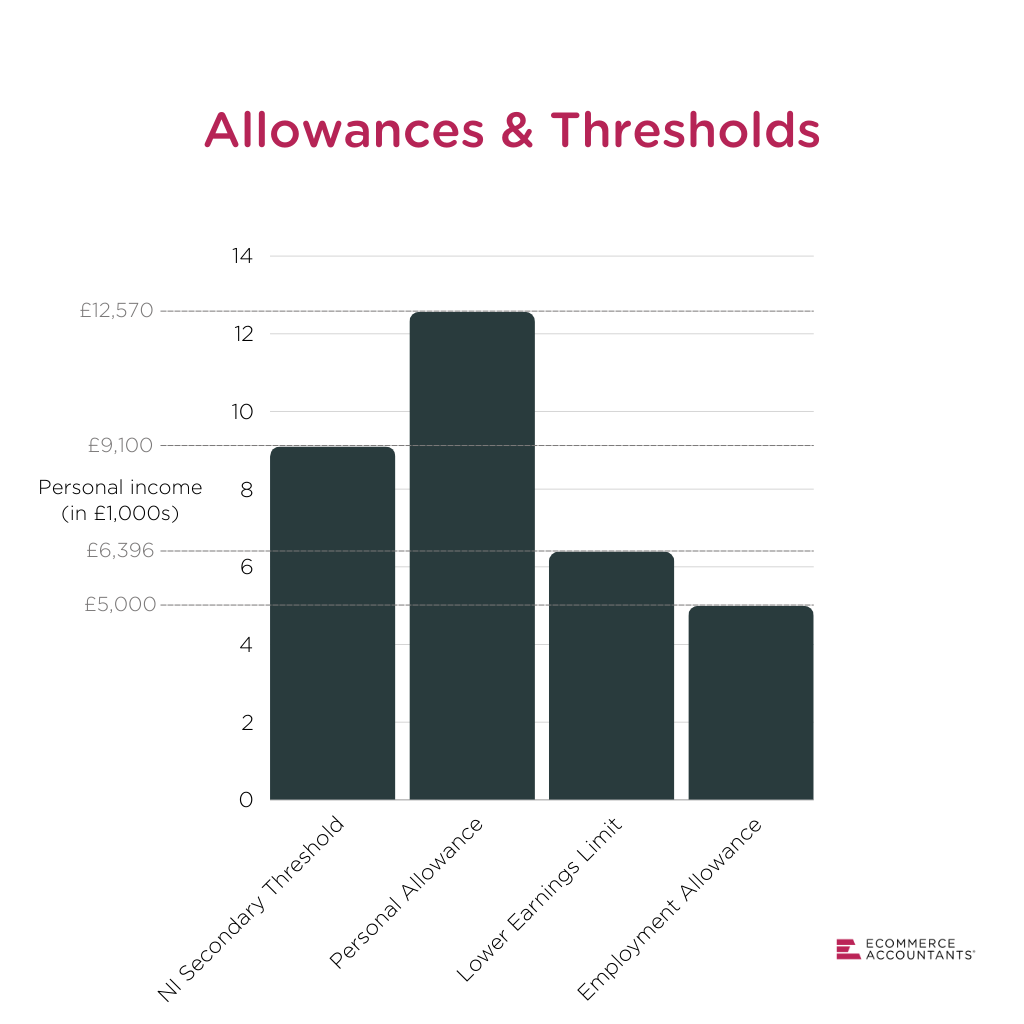

Allowances and Thresholds for 2024/25

What is the Personal Tax Allowance for 2024/25?

Your earnings below this threshold will not be subject to personal income tax. For England, Northern Ireland and Scotland, the standard personal tax allowance for the 2024/25 tax year is:

- £242 per week

- £1,048 per month

- £12,570 per year

What is the Class 1 National Insurance Secondary Threshold for 2024/25?

Your earnings below this threshold will not be subject to Employee or Employer National Insurance contributions. The Class 1 National Insurance Secondary Threshold for the 2024/25 tax year is:

- £175 per week

- £758 per month

- £9,100 per year

What is the Lower Earnings Limit for 2024/25?

Provided you earn a salary above this limit, this will count as if you are making National Insurance contributions and you will receive the associated benefits. The Lower Earnings Limit for 2024/25 is:

- £123 per week

- £533 per month

- £6,396 per year

What is the Employment Allowance for 2024/25?

Employment Allowance allows you, as an eligible employer, to reduce your annual National Insurance liability by up to the annual allowance. For the 2024/25 tax year the allowance is:

- £5,000

What is the most tax efficient directors salary 2024/25?

With the thresholds in tow, we can now tackle this question and the answer depends on the number of staff you currently employ.

I am a sole director (1 employee)

As a sole director, you have 2 primary options, you can pay yourself either:

- The Personal Tax Allowance £12,570 per annum

- The Class 1 National Insurance Secondary Threshold of £9,100 per annum, or

Pay yourself the Secondary Threshold (Mix 1)

Shown as Mix 1 on the graph, paying yourself £758.33 per month amounts to an annual salary of £9,100. This matches the Secondary Threshold (£9,100) which means that:

- You don’t have any personal tax obligations

- You don’t have any Employee or Employer National Insurance obligations

The remainder of your income could be issued via dividend payments.

Pay yourself the Personal Tax Allowance (Mix 2)

Shown as Mix 2 on the graph, paying yourself £1,047.50 per month amounts to an annual salary of £12,570. This matches the Personal Tax Allowance which means that:

- You don’t have any personal tax obligations

- You do have an Employer National Insurance obligation of £478.86

The remainder of your income could, once again, be issued through dividend payments.

Note, your Employer National Insurance obligation of £478.86 will be offset by increased corporation tax savings. This is because instead of paying yourself £9,100 with no obligations, you increase this by £3,470 to £12,570 and that incurs £478.86 of Employer National Insurance. Therefore, your company's salary expense is increased by a total of £3,948.86 (£3,470+£478.86), meaning that your corporation tax will be reduced by £750.28 (£3,948.86 X 19%).

This is assuming that your annual company profits are £50,000 or less. If your profits are higher, then your corporate tax savings will also increase.

Although paying yourself £12,570 may result in a greater tax saving, some opt to pay themselves £9,100 in order to avoid the payroll liabilities altogether. If you’re already a payroll client of ours, we recommend paying yourself the higher amount because we will stay on top of any obligations for you. If you would like our help with this, get in touch with us today.

My company has 2 directors or 1 additional employee (or more)

If you have 2 or more directors or 1 additional employee then you may be eligible for Employment Allowance (more on this below). In such a case, paying yourself £1,047.50 per month (£12,570 per annum), which matches the Personal Tax Allowance (Mix 2), will be the most efficient salary because your Employer National Insurance will be covered. In this scenario:

- You don’t have any personal tax obligations

- You don’t have any Employee or Employer National Insurance obligations

Frequently asked questions

Will I still qualify for state pension and other benefits?

In all the above cases, yes. Even though you may not be making National Insurance contributions, if you have a salary above than the Lower Earnings Limit (LEL), which is £533 per month (£6,396 per annum), this will still count as if you are making contributions. This means you will still receive the benefits associated with making the contributions.

What is Employer National Insurance?

Employer National Insurance is another form of tax levied on earnings and this is paid by an employer. For 2024/2025, the rate is set at 13.8% of earnings that are above secondary threshold of £9,100 per annum.

Can I use Employment Allowance for 2024/2025?

To qualify for the allowance this year (2024/2025), your total Employer Class 1 National Insurance liability must have been less than £100,000 in the prior tax year (2023/2024).

It is important to note, however, that you cannot claim the Employment Allowance if your company only has 1 employee who is paid above the Class 1 National Insurance secondary threshold (£9,100) and that employee is a director. In short, if you’re a sole director paid above this, you cannot apply the allowance to your payroll. Learn more on the government’s page where they break down employment allowance eligibility.

If you want to freshen up on the basics of payroll, see our UK payroll explained post.

Last word

In summary, the best way for you to pay yourself in the 2024/2025 year is through a mix of salary and dividend payments. The best director salary 2024/25 is either £9,100 or £12,570 depending on the number of employees and your personal preference. The remainder of your income coulde be in the form of dividend payments, leveraging the lower dividend tax rates. You can learn more about dividends here. That concludes our post on the most tax efficient directors salary 2024/25. If you're looking for an accountant who understands your business, get in touch with us today.

.webp)

.png)

%20(1).png)